Imagination and the Future of Cryptocurrency

Published 8 October 2021

By Dr Peter J Phillips, Associate Professor (Finance & Banking) University of Southern Queensland

Decision theory or the economics of information sits at the very heart of modern finance theory. Keep digging beneath the computers and the data and the algorithms and you will find it. Emerging with full vigour in the mid-20th century, decision theory is a set of rules and methods designed to identify the optimal ordering of alternatives. If you must decide between A and B and C and D, decision theory says that you should figure out the outcomes (x’s) that might be experienced by choosing one of the alternatives and the probabilities (p’s) of those outcomes occurring. You can use this information to rank the alternatives best to worst, most likely using expected utility (rational choice) theory as the “calculator”.

Ideally, the investor would go through such a process when selecting individual assets or portfolios. In fact, the Markowitz Modern Portfolio Theory that we have referenced in previous posts embeds such a process (approximately).

With established risky assets like equities and bonds, there is so much historical data that the investor could, if so inclined, start with the averages and standard deviations of returns, assume a normal or lognormal probability distribution, and begin to build a picture of a possible future from that statistical foundation.

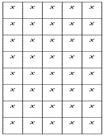

The orthodox decision theorist would, in fact, delineate the problem space such that averages + standard deviations + a probability distribution are the three things that are used to determine each possible outcome and its associated probability. This net has holes in it, but what is not captured is ignored. We might picture this as a “closed” space, containing all the outcomes (x’s) that are deemed possible by taking this approach:

While this is the orthodox approach prescribed by decision theory, it is clearly the case that other factors are at play when people are making decisions. The world is risky, but it is also characterised by uncertainty. A risky prospect is one where you can, at least in principle, depict the outcomes in the manner just described. There are no unknown x’s and the probabilities (p’s) that are attached to each outcome sum to one. There is nothing left over. This situation may encompass games of chance but how does it fare in an open, non-delineated world?

An uncertain, open, non-delineated world is one where there are unknown x’s or where, if the x’s are known, it is not possible to attach a probability to them. In such a world as this, our theories of decision must be adapted, and potentially radically changed.

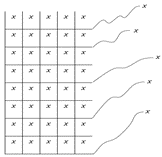

Perhaps the most radical of all the mid-20th century economists working in this field was George Shackle. His work has fascinated economists for decades. Unlike his contemporaries, Shackle stresses the importance of imagination, and he replaces probability with a measure of uncertainty that he calls potential surprise. Shackle’s decision-maker faces an open, non-delineated world, where x’s can be imagined and, together with how surprising it would be if they were to occur, impact the decision-maker’s deliberations with varying degrees of intensity. Shackle problem space looks more like this:

I have written about Shackle elsewhere if you’re interested in learning more (see below). The important thing to consider here is the cryptocurrency decision-making context. It is entirely likely that many sophisticated traders are applying decision theoretic concepts like Markowitz’ methods to guide their trades. It almost certainly the case that for many traders, the open problem space depicted by Shackle is a more accurate representation. The future of cryptocurrency can be imagined differently. The intensity of the imaginative experience will be different for each potential investor. As a result of such deliberations, some will take the plunge into cryptocurrency. Others will not. Perhaps more important than these decisions are the decisions that are yet to come. These include decisions by merchants to accept cryptocurrency, decisions by banks and payment platforms, and regulators. Together, these decisions will determine a world with or without cryptocurrency. What world do you imagine?

Discussion Questions

Lots of people know someone who trades cryptocurrency. What guides their decision-making? Are they traders or have they imagined a long-term future with or without cryptocurrency?

Further Reading

See my Shackle’s Decision Order and Time, A Reader’s Guide. One way of viewing some of the concepts in the textbook is as decision-making structures. The way that bond prices move and the formulas that are used to price them contain important insights into the nature of the bond market that are essential for making good decisions. The same is true for the other markets and instruments that we cover throughout the text.

Read other posts

Free Cash Flow: The Driver of Shareholder Value

Australia’s New Tech Index: A Local Version of the NASDAQ?

The Behavioural Economics of ‘Going on Tilt’

A Cup of Coffee and an Option Pricing Model

Yes Virginia, there is a Mortgage Tipping Point

How Universities Shape the Real World: The Case of Corporate Finance

Disinformation: Can is Sweep Investors off their Feet?

Hedge Funds, Satellites and Empty Carparks

The Battle for FinTech Supremacy: The Tech Titans Vs the Masters of the Universe

Algorithms in Finance? That's Nothing New

The Algorithm that finds the ‘Best’ Portfolio

Why you should study Finance and Economics in the 21st Century

From Chicago to New York: Futures Trading and Microwave Popcorn

Basketball, Fund Managers, and the Hot Hand

The French Connection in Finance Theory

The Road to Cryptocurrency, Instalment # 1

The Road to Cryptocurrency Instalment #2

The Road to Cryptocurrency Instalment #3

The Road to Cryptocurrency Instalment #4

The Road to Cryptocurrency Instalment #5

The Road to Cryptocurrency Instalment #6

The Road to Cryptocurrency Instalment #7